Follow @solverworld Tweet this

“All about X, part 1” is really a fancy way of saying a little bit about X.

How do you eat an elephant?

One bite at a time 1

So let’s eat stochastic difference equations one bite at a time. Let’s consider a first-order linear equation driven by a Gaussian random variable.

\begin{align}

x_{n+1}&=ax_n+w_n \\

w_n &\sim N(0, \sigma^2) \\

|a| & < 1. \\

\end{align}

Let’s dissect this one bit at a time. \(x_n \) is our system’s state, or value, at time \(n \). Our time variable \(n \) takes on integer values, -2, -1, 0, 1, 2, and so on. \(w_n\) is our noise term, and it is a normally distributed Gaussian variable with mean 0 and standard deviation \(\sigma\) at each time \(n\). The values at different times are uncorrelated. We require \(|a|<1\) so that our equation is stable, or does not blow up.

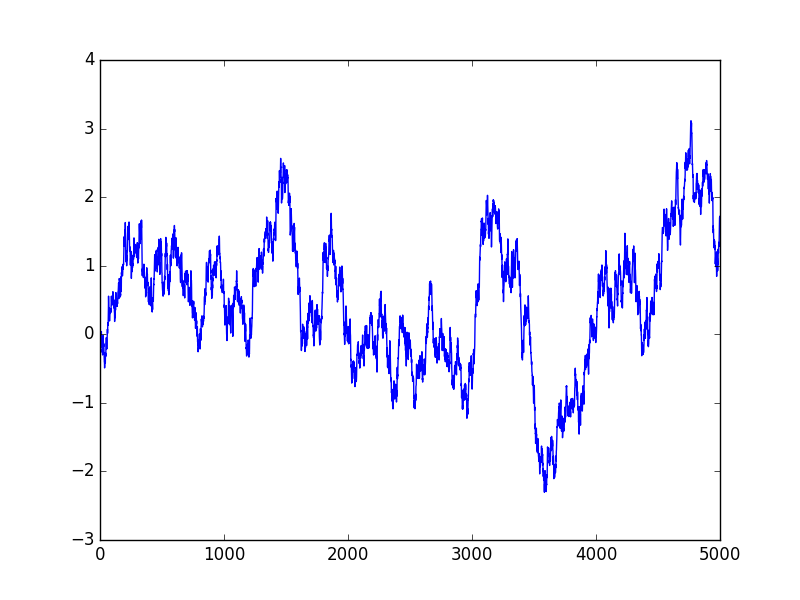

What does this series look like? Here is a sample run of 5000 steps for a=0.9967 and \(\sigma=\)0.082. The significance of these numbers will be revealed later.

Let’s derive some basic properties of our stochastic series \(x_n\). Recall that \(E()\) is the expectation operator, meaning it computes the expected value of its random variable argument.

\(\newcommand{\Var}{\mathrm{Var}}\)

\(\newcommand{\Cov}{\mathrm{Cov}}\)

\(\newcommand{\Expect}{{\rm I\kern-.3em E}}\)

What is the average (expected) value of \(x_n\)? Since our process is stationary, that is, a is fixed, and \(w_n\) does not varying it’s statistics over time, \(\Expect(x_n)\) is constant, let’s call it \(\Expect(x)\). Then

\begin{align}

\Expect(x_{n+1})&=a\Expect(x_n)+\Expect(w_n) \\

\Expect(x)(1-a)&=\Expect(w_n) \\

\Expect(x)&=0

\end{align}

where we used \(E(w_n)=0\) for the final step.

What about the variance of x?

\begin{align}

\Var(x_{n+1})&=a^2\Var(x_n)+\Var(w_n) \\

\Var(x)(1-a^2)&=\sigma^2 \\

\Var(x)&=\frac{\sigma^2}{1-a^2}

\end{align}

\begin{align}

\Cov(x_{n+1},x_n)&=\Expect[(x_{n+1}-\Expect(x_{n+1}))(x_{n}-\Expect(x_{n}))]\\

&=\Expect[x_{n+1}x_{n}]\\

&=\Expect[(ax_n+w_n)x_n]\\

&=\Expect[ax_n^2]\\

&=\frac{a\sigma^2}{1-a^2}

\end{align}

Let’s look at the increments:

\begin{align}

\Delta x_{n+1}&=x_{n+1}-x_n\\

&=(a-1)x_n+w_n\\

\Var(\Delta x)&=(a-1)^2\Var(x)+\sigma^2\\

\Var(\Delta x)&=\sigma^2[\frac{(1-a)^2}{1-a^2}+1]\\

&=\sigma^2\frac{2}{1+a}.

\end{align}

Note If a is close to 1, then the variance of the increments is close to \(\sigma^2\).

Now, let’s get a little more involved and compute the variance over k steps. From some basic system theory (or inspection):

\begin{align}

x_k=x_0 a^k + \sum_{s=0}^{k-1}a^{k-s-1}w_s

\end{align}

To make sure we have the right limits, let’s check for k=1:

\[

x_1=a x_0 + w_0

\]

That looks right, let’s continue on.

\begin{align}

\Var(x_k-x_0)=(a^k-1)^2\Var(x)+\sigma^2\sum_{s=0}^{k-1}(a^{k-s-1})^2

\end{align}

Now, using the Sum of a Geometric Series, we have

\begin{align}

\Var(x_k-x_0)&=\frac{(a^k-1)^2}{1-a^2}\sigma^2 + \frac{1-a^{2k}}{1-a^2}\\

&=\sigma^2 [ \frac{(a^k-1)^2 + 1 – a^{2k}}{1-a^2}\\

&=2 \sigma^2 \frac{1-a^k}{1-a^2}.

\end{align}

Checking when \(k=1\) and we see it matches our earlier result.

In Part 2 we will look more closely at some simulations and trading results on these series.